In April 2026, PayPal added support for sending ETH directly from its app to any Ethereum wallet address. Travala lets you book over three million hotels in ETH. Chipotle has been accepting crypto payments through Flexa since 2022. ETH payment has moved well past the “coming soon” phase. The question is no longer whether you can pay with Ethereum but where it makes sense, how the fees work, and what you actually need to do it. This guide covers all of that without the hype.

What Is an ETH Payment?

An ETH payment is a transfer of Ether from one Ethereum wallet to another, recorded permanently on the blockchain. Unlike a bank transfer, there is no intermediary. The sender initiates the transaction from their wallet, the Ethereum network processes it, and the recipient’s wallet receives the funds. No bank approves or rejects it. No account can be frozen between the two parties. The transaction history is public and cannot be altered.

How ETH payment differs from a bank transfer

A bank transfer moves a number in a bank’s database from one account to another. The bank is the trusted third party that makes that possible. An Ethereum payment moves value recorded on a decentralized blockchain where no single entity controls the ledger. The practical differences matter: ETH transfers work 24 hours a day, seven days a week, including public holidays. There are no geographic restrictions. You do not need to provide any personal information beyond a wallet address. And once a transaction is confirmed, it cannot be reversed by any party, which is an advantage for merchants and a responsibility for senders.

One characteristic that surprises people new to paying with Ethereum is that sending ETH requires paying a gas fee in ETH on top of the amount being sent. If you want to send $100 worth of ETH, you need enough ETH for the $100 plus the gas fee. That fee goes to the validators who process the transaction, not to any company. The full mechanics of how Ethereum gas fees work explains why fees vary and how to keep them manageable.

ETH vs stablecoins for payments – which one actually makes sense

There is an important distinction between paying in ETH and paying on the Ethereum network. When you pay a merchant in USDC or USDT, you are using the Ethereum network as the settlement layer, but you are transacting in a token pegged to the US dollar. No price volatility. When you pay in ETH itself, the recipient receives an asset whose value changes continuously.

Many merchants who technically accept Ethereum payments are actually accepting USDC or USDT settled on Ethereum. For buyers who want certainty about how much they are spending, stablecoins make more practical sense for everyday purchases. ETH as a direct payment currency makes more sense for larger purchases where both parties are comfortable with some price variation, or where the merchant uses a payment processor that auto-converts ETH to fiat at the moment of transaction.

How ETH Payment Works – From Wallet to Confirmation

The mechanics of an ETH payment are straightforward once you understand what each step actually does.

The payment flow – what happens when you pay with ETH

- You open your wallet – MetaMask, Coinbase Wallet, Trust Wallet, or any compatible Ethereum wallet.

- You enter the recipient’s wallet address or scan their QR code. Always verify the address character by character – clipboard-hijacking malware exists that replaces copied addresses silently.

- You enter the amount in ETH. Your wallet shows the equivalent in fiat at current prices.

- You review the gas fee estimate. Your wallet lets you choose between slow (cheaper), standard, and fast (more expensive) confirmation speeds.

- You confirm the transaction. Your wallet signs it with your private key.

- The signed transaction is broadcast to the Ethereum network, where validators pick it up and include it in the next block.

- After one block confirmation (roughly 12-15 seconds), the transaction appears as pending in the recipient’s wallet. After roughly 2-5 minutes and a few more block confirmations, most merchants consider it settled for online purchases.

Confirmation time – initial vs finality

The word “confirmation” means different things depending on context. A single block confirmation happens in roughly 12-15 seconds and is enough for low-value online transactions where merchants are comfortable with minimal risk. Most online stores using payment processors treat a transaction as complete after 2-5 minutes and a handful of confirmations.

Economic finality on Ethereum takes approximately 15 minutes, or 32 blocks. This is the point at which the transaction is considered irreversible under the protocol’s consensus rules. For large purchases like property or high-value equipment, waiting for full finality before releasing goods is the appropriate standard. For a coffee or a domain name purchase, one or two confirmations is more than sufficient. The gap between initial and full confirmation is why paying with ETH in a physical store at checkout is impractical on mainnet without Layer 2 underneath it.

Gas fees – the real cost of every ETH payment

Every Ethereum transaction costs gas, measured in gwei (one billionth of one ETH). A simple ETH transfer uses 21,000 units of gas. More complex interactions with smart contracts use more. The total fee is gas used multiplied by the current gas price, which fluctuates with network demand.

On mainnet, gas fees have ranged from under $0.10 during quiet periods to over $50 during periods of high congestion. This fee structure creates a practical problem for small payments: if a gas fee costs $3 and your purchase costs $5, you are effectively paying 60% overhead. This is the main argument against using Ethereum mainnet for everyday purchases below $100, and it is exactly the problem that Layer 2 networks solve. To understand how Ethereum works at the level that produces these fees, the basics of transaction processing and block inclusion clarify why costs behave the way they do.

Layer 2 Networks: The Fix for ETH Payment Limitations

The common objections to ETH as a payment method – slow confirmation, unpredictable fees, impractical for small amounts – all apply specifically to Ethereum mainnet. Layer 2 networks address all three.

Why mainnet ETH is not ideal for everyday payments

A $3 gas fee on a $20 purchase is a 15% overhead. Waiting 15 minutes for full finality at a checkout counter is not realistic. These are genuine limitations of Ethereum mainnet, and critics of ETH as a payment method are correct to point them out when the discussion stays at the mainnet level. The Ethereum network was not optimized primarily for micropayments. It was optimized for security and decentralization. Layer 2 networks are where the payment use case actually becomes practical.

How Arbitrum, Base, and Optimism change the picture

Layer 2 networks like Arbitrum, Optimism, and Coinbase’s Base process transactions off the main Ethereum chain and post compressed batches back to mainnet for settlement. The result is fees below $0.01 for most transactions and confirmation times of 2-3 seconds. The same MetaMask wallet you use on mainnet works on these networks without any changes. You just switch the network setting in the wallet.

Base, launched by Coinbase in 2023 and significantly expanded through 2025 and 2026, has become the largest consumer-facing Layer 2 by active users. Its integration with ENS naming means sending to someone’s name.base.eth is as simple as sending an email. The Ethereum Name Service works across these networks, giving wallets readable identifiers rather than 42-character addresses. To understand the naming layer that makes this work, the guide on the Ethereum Name Service covers how .eth names resolve to wallet addresses. Moving funds from mainnet to a Layer 2 network to take advantage of lower fees is covered in the guide on bridging ETH to layer 2.

ETH payment on Layer 2 – practical examples

Flexa operates a payment network that settles transactions in crypto, including ETH, for physical retail merchants. When you pay with ETH at Chipotle through Flexa, the confirmation happens in seconds and the merchant receives fiat. You pay in crypto, they receive dollars, and the settlement happens on-chain in the background. AMC Theatres uses the same system. For the customer, it works like tapping a card. For the merchant, it settles like a bank transfer with lower fees and no chargeback risk.

Base App, Coinbase’s consumer interface for its Layer 2, launched in July 2025 with integrated ETH payment functionality for peer-to-peer and merchant transfers. Transaction costs on Base run under $0.01, confirmations happen in 2-3 seconds, and the interface is designed for users who have never interacted with blockchain infrastructure directly.

Benefits of Paying with ETH – For Buyers and Sellers

The advantages of ETH as a payment method differ depending on which side of the transaction you are on. Buyers and merchants have different reasons to prefer it over traditional payment rails.

Benefits for individuals paying with ETH

- Cross-border payments with no currency conversion: Sending ETH to a merchant in Japan, Brazil, or Germany costs the same as sending it next door. No forex fees, no correspondent bank fees, no multi-day processing time.

- No need to share bank details: You give the merchant your transaction hash as proof of payment. Your bank account number, routing number, and billing address stay private.

- 24/7 availability: Banks close. Ethereum does not. International transfers that would take three business days through SWIFT clear in minutes via ETH.

- Self-custody: Your funds sit in your own wallet, not in a bank that can freeze your account or fail. You control access with your private key.

- Lower fees for international transfers: SWIFT international transfers can cost $25-50 per transaction. An ETH transfer on Layer 2 costs under $0.01.

Benefits for merchants accepting ETH

- No chargebacks: Once an ETH transaction is confirmed, it cannot be reversed. Credit card chargebacks cost merchants an average of $3.75 per $1 disputed, plus the disputed amount. ETH eliminates this entirely.

- Lower processing fees: Visa and Mastercard charge merchants 1.5-3.5% per transaction. Ethereum payment processors typically charge 0-1%, with the gas fee paid by the customer.

- Instant settlement: Card payments take 1-3 business days to settle in a merchant’s bank account. ETH settles in minutes. For cash flow, this is a real operational advantage.

- Global customer base without geographic restrictions: A US merchant can accept payment from anyone in the world without currency conversion overhead or payment processor country blocks.

- Smart contract automation: Recurring payments, conditional releases, and multi-party payment splits can be built directly into the payment logic without a third-party subscription manager.

ETH vs credit card payments – direct comparison

| Feature | ETH Payment | Credit Card |

|---|---|---|

| Transaction fee | 0-1% (plus gas) | 1.5-3.5% |

| Chargeback | Not possible | Possible (fraud risk for merchants) |

| Settlement time | Minutes to hours | 1-3 business days |

| Geographic limits | None | Sometimes restricted by country |

| Requires bank account | No | Yes |

| Volatility risk | Yes (mitigated by stablecoins) | No |

| Available 24/7 | Yes | Dependent on processor uptime |

Who Accepts Ethereum as Payment in 2026?

The list of merchants accepting ETH has grown from a handful of crypto-native platforms to mainstream retailers, travel companies, and financial services. Here is a breakdown by category.

Major retailers and e-commerce

- Overstock: One of the first major US retailers to accept crypto. Accepts ETH directly for furniture, electronics, and home goods.

- Newegg: Electronics and computer components in ETH and other cryptocurrencies. Popular with the tech-savvy buyer who prefers crypto over cards.

- Crypto Emporium: Luxury goods, vehicles, and high-value items. Accepts ETH directly for purchases ranging from watches to cars.

- Shopify merchants: Thousands of individual stores on Shopify accept ETH through payment processor integrations. There is no single Shopify ETH switch – individual merchants enable it through Coinbase Commerce, BitPay, or similar processors.

Travel and accommodation

Travala is the clearest example of ETH acceptance at scale in the travel sector. Over three million hotels, flights, and activities are bookable directly in ETH, with no conversion step required at checkout. The platform has its own loyalty token but ETH is a primary accepted currency. For international bookings, paying in ETH avoids the foreign transaction fees that credit cards charge (typically 1-3%), which on a $2,000 hotel booking adds up to meaningful savings. Travala also accepts other cryptocurrencies, making it the most crypto-friendly booking platform available in 2026.

Food, entertainment, and gaming

Chipotle began accepting crypto through Flexa in 2022 alongside the “Proof of Steak” campaign tied to Ethereum’s transition to Proof of Stake. AMC Theatres added crypto payment support through the same period. In both cases, the infrastructure is Flexa: the customer pays in ETH, the merchant receives fiat, and Flexa handles the settlement on-chain. The crypto remains in the payment rail, but the merchant never holds a volatile asset.

Gaming is where ETH payments have the deepest integration. NFT-based games, digital collectible platforms, and blockchain gaming marketplaces handle ETH natively. Gods Unchained, Axie Infinity, and Sorare all operate with ETH as the primary transaction currency for card purchases, breeding, and marketplace trades.

Real estate and high-value purchases

Propy runs a blockchain-based real estate platform where property deeds can transfer on-chain, with ETH used for the purchase transaction. Pacaso, which sells fractional vacation home ownership, accepts ETH for property stakes. Crypto Emporium lists residential and commercial real estate for direct ETH purchase. For large transactions, ETH’s irreversibility and speed compared to wire transfers are genuine advantages: a $500,000 wire transfer through SWIFT takes 3-5 business days and costs hundreds in fees. The equivalent ETH transfer settles in minutes with lower overhead.

Financial services and online platforms

PayPal added native ETH support in April 2026, allowing users to send ETH directly from their PayPal balance to any Ethereum wallet address. This was a significant step because PayPal’s 400 million active users can now transact in ETH without touching a crypto exchange. Robinhood offers integrated ETH wallets. Twitch streamers receive ETH donations and tips. Domain registrars Namecheap and Namesilo accept ETH for domain purchases. For an overview of the full range of things ETH is used for beyond payments, the breakdown covers DeFi, staking, and the other major use cases alongside the payment function.

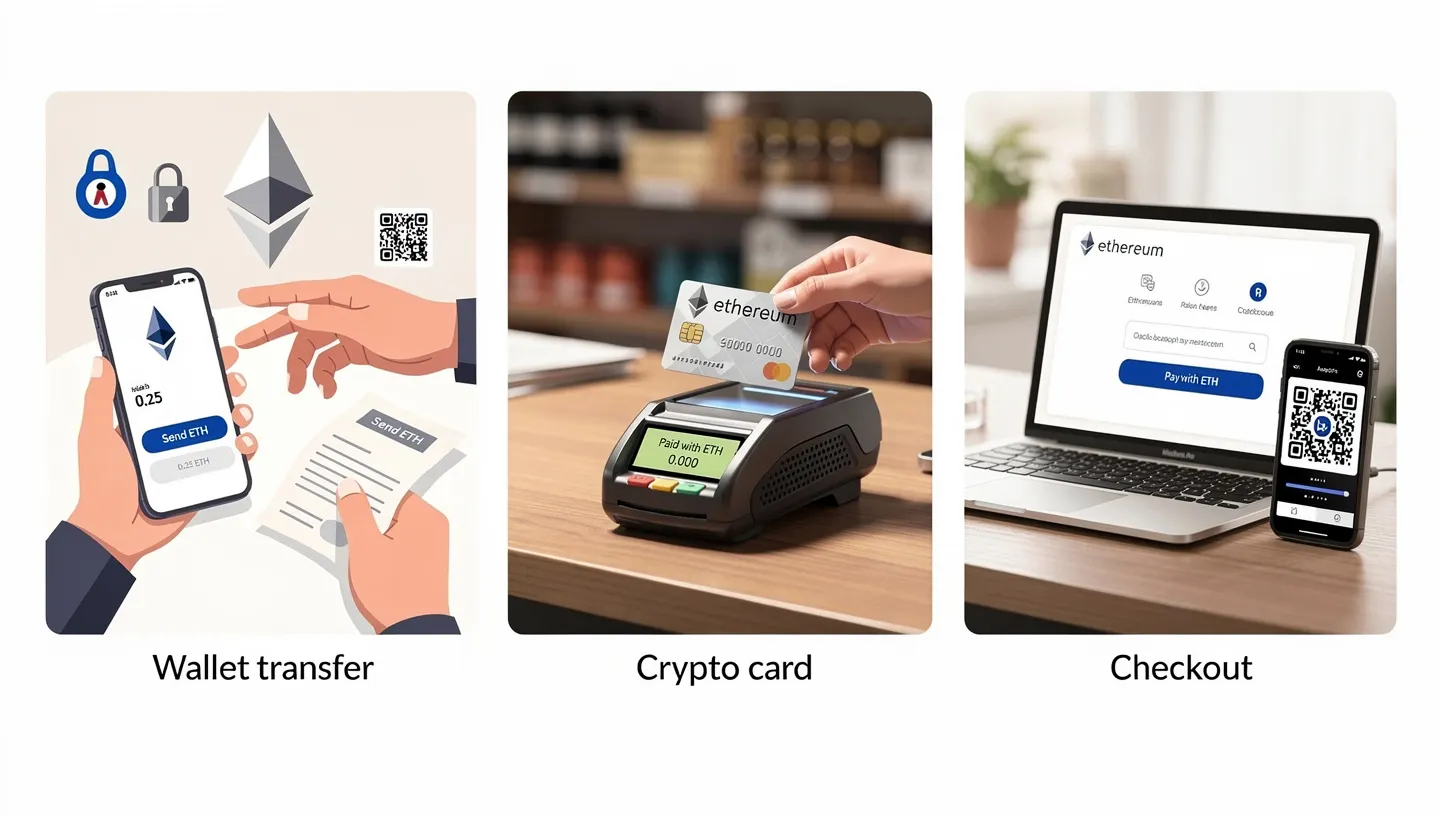

How to Pay with ETH – Step by Step

Three methods cover the practical ways to make an ETH payment: direct wallet transfer, crypto debit card, and payment processor checkout.

Method 1 – Direct wallet transfer

- Set up a wallet. MetaMask is the most widely used for Ethereum. Coinbase Wallet and Trust Wallet are solid alternatives. Each generates a wallet address you own and control.

- Buy ETH on an exchange and send it to your wallet, or transfer ETH you already hold. The guide on how to buy Ethereum covers the purchase process from exchange selection through to wallet transfer.

- Get the merchant’s wallet address or QR code. Most ETH-accepting merchants display a QR code at checkout or in their payment instructions.

- In your wallet, select Send. Paste the address or scan the QR code. Compare the first six and last six characters of the pasted address against what the merchant showed you – clipboard malware that swaps addresses mid-paste is a documented threat.

- Enter the amount. Add a small buffer above the quoted price to cover gas fee variation, or confirm the exact gas cost shown by your wallet before sending.

- Confirm the transaction. Save the transaction hash that appears afterward as your proof of payment.

Method 2 – Crypto debit card

A crypto debit card converts your ETH or other crypto holdings to fiat at point of sale, letting you pay anywhere Visa or Mastercard is accepted. Coinbase Card, Crypto.com Visa, and Binance Card all work this way. You load the card from your crypto holdings, and when you pay, the crypto is converted at the current rate and the merchant receives fiat. The advantage is universal merchant acceptance. The tradeoffs are a conversion fee (typically 0.5-2.5%) and the fact that you are converting your ETH to dollars at the time of the purchase, which closes out your position in that asset at that moment.

Method 3 – Payment processor at checkout

When a merchant integrates a crypto payment processor, you see ETH as a checkout option alongside card and PayPal. You select it, the processor displays a QR code or wallet address with a specific amount and a time limit (usually 15-20 minutes), and you send the ETH from your wallet. The processor confirms the transaction on-chain and notifies the merchant. Most processors offer automatic fiat conversion so the merchant receives their local currency rather than holding ETH. This is the path Overstock, Newegg, and Shopify merchants use.

Risks and Limitations of ETH Payments

Using ETH as a payment method has real drawbacks alongside the advantages. Understanding them helps you decide when ETH payment is the right tool and when a card or stablecoin makes more sense.

Price volatility – and how to manage it

ETH can drop 10-20% in a single day. If you pay 0.5 ETH for something worth $1,000 today and ETH falls 20% tomorrow, you effectively overpaid by $200 relative to what the merchant received. For merchants, the same swing can turn a profitable sale into a loss if they hold ETH rather than converting it immediately.

The practical solutions: merchants should use payment processors with auto-conversion to fiat at the moment of transaction. Buyers who want price certainty should pay in USDC rather than ETH for everyday purchases. ETH as a direct payment currency makes the most sense for buyers who are comfortable spending it at current prices and not tracking whether it would have been worth more next week.

Gas fee unpredictability

Gas fees on Ethereum mainnet are not fixed. During quiet periods, a basic ETH transfer costs under $0.50. During high network activity – major NFT drops, market volatility events, protocol launches – that same transfer can cost $20 or more. For time-sensitive payments, spiking gas makes budgeting difficult. The solutions are to use Layer 2 networks for routine payments, to use ETH Gas Tracker on Etherscan to check current gas prices before sending, and to set a maximum gas limit in your wallet so you are not charged more than you intended if prices spike while your transaction is pending.

Irreversibility – no chargeback protection for buyers

No chargeback is an advantage for merchants and a risk for buyers. If you pay for something and the merchant does not deliver, or delivers something different from what was described, you have no payment network to dispute the charge with. The only recourse is direct negotiation with the merchant or, in some cases, legal action. For purchases from established retailers with clear return policies, this is a manageable risk. For purchases from unknown parties or in markets where fraud is common, it demands more caution than a card payment would.

For large transfers, send a small test transaction first. Verify the address resolves to who you expect it to. Confirm the amount before signing, not just before initiating. Once confirmed on the blockchain, the transaction cannot be undone by any party. The broader landscape of how Ethereum’s security model works and what Ether actually is at the protocol level gives useful context for understanding why these properties are fundamental rather than fixable.

Regulatory considerations in 2026

In the EU, the MiCA (Markets in Crypto-Assets) regulation that came fully into force in 2024 has created compliance obligations for businesses that regularly accept or process crypto payments. Merchants above certain transaction thresholds may have AML (anti-money laundering) and KYC (know your customer) obligations depending on their jurisdiction and the size of crypto payments they receive.

For individuals, using ETH to pay for goods and services may trigger a taxable event in most jurisdictions. In the United States, the IRS treats spending cryptocurrency as a disposal of an asset. If you bought ETH at $1,000 and spend it when it is worth $3,000, you have realized a $2,000 capital gain that is reportable. This applies regardless of whether the purchase was a coffee or a car. Consulting a tax professional before using ETH regularly for purchases is the appropriate step for anyone in a jurisdiction where crypto is a taxable asset.

How to Accept ETH as a Merchant

Setting up ETH payment acceptance ranges from a two-minute job to a technical integration project, depending on how much control you want over the process.

Payment gateway options – Coinbase Commerce, BitPay, and NOWPayments

| Payment Processor | Fee | Auto Fiat Conversion | Platform Plugins |

|---|---|---|---|

| Coinbase Commerce | 0% | Yes | Shopify, WooCommerce |

| BitPay | 1% | Yes | WooCommerce, Magento |

| NOWPayments | 0.5% | Yes | 20+ integrations |

| Flexa | 0.5% | Yes | In-store POS terminal |

Coinbase Commerce charges no platform fee and integrates directly with Shopify and WooCommerce through official plugins. For a small business with an existing online store, it is the lowest-friction path to accepting ETH. BitPay has a longer track record and wider fiat conversion options across more currencies. NOWPayments supports the broadest range of cryptocurrencies and has the most platform integrations of the three. Flexa is the only option built specifically for physical retail point-of-sale, where in-person QR code scanning is the payment method.

Simple setup for small businesses

The three-option spectrum for small merchants: the simplest is a static wallet address displayed at checkout or on an invoice, with customers sending ETH directly and the merchant checking transaction confirmations manually. No third party, no fees, but also no auto-conversion and no integrated receipt system. The middle option is Coinbase Commerce with a Shopify or WooCommerce plugin, which handles confirmation tracking, receipt generation, and optional fiat conversion automatically for a 0% platform fee. The most automated option is a payment API integration, where ETH payment is embedded directly in a custom checkout with smart contract logic handling receipts, refunds, and conversion. The smart contract infrastructure that powers these payment automations is the same infrastructure underlying DeFi and token transfers.

Smart contract recurring payments

One capability that ETH payments have over traditional payment rails is programmable recurring payments through smart contracts. Rather than storing a card number and billing it monthly through a payment processor, a subscription model can be implemented where the customer approves a one-time permission for a contract to withdraw a specified amount of ETH or USDC monthly. The contract executes automatically on schedule with no manual intervention from either party. Protocols like Sablier enable streaming payments – a salary or subscription paid continuously by the second rather than in monthly lump sums. Request Network handles invoice-based crypto payment flows with on-chain audit trails. These tools remain niche in 2026 but represent a payment model that has no equivalent in traditional finance.

ETH vs Bitcoin vs PayPal: Which Payment Method Wins?

No single answer fits every situation. The comparison depends on what matters most to you: speed, cost, merchant acceptance, or programmability.

ETH vs Bitcoin for payments

| Feature | ETH (mainnet) | ETH (Layer 2) | Bitcoin |

|---|---|---|---|

| Confirmation time | 12-15 seconds | 2-3 seconds | ~10 minutes |

| Transaction fee | $0.10-$50+ | Under $0.01 | $1-$50+ |

| Smart contracts | Yes | Yes | Limited |

| Programmability | Full | Full | Minimal |

| Merchant acceptance | Growing | Growing | Wider (currently) |

Bitcoin currently has wider merchant acceptance because it has been around longer and many crypto payment integrations added Bitcoin first. On the payment mechanics, ETH mainnet and Bitcoin are comparable in terms of fee unpredictability. ETH on Layer 2 wins on both speed and cost. For payments that require any kind of programmability – recurring billing, conditional release, escrow – Ethereum is the only practical option. Bitcoin’s scripting language does not support the smart contract functionality that makes those payment structures possible. The guide on what Ethereum is and how it differs from Bitcoin as a platform covers the architectural differences that produce these payment-relevant distinctions.

ETH vs PayPal for international payments

PayPal charges a currency conversion fee of 3-4% for international transactions, takes 1-3 business days for cross-border settlement, and restricts availability by country. Countries without PayPal access cannot receive PayPal payments at all. ETH on Layer 2 charges under $0.01 for any transfer regardless of destination, settles in 2-3 seconds, and has no country restrictions. Anyone with a wallet address can receive ETH regardless of where they are or what financial infrastructure exists in their country.

PayPal wins on consumer protection – chargebacks exist, disputes can be raised, and the platform has enforcement mechanisms. ETH wins on cost and access for international transfers. PayPal’s April 2026 addition of native ETH sending is significant because it bridges the two: PayPal users can now send ETH to any Ethereum address from the PayPal interface without interacting with a crypto exchange directly.

Frequently Asked Questions

What is ETH payment?

ETH payment is the use of Ether, Ethereum’s native cryptocurrency, to pay for goods, services, or transfers. The transaction goes directly from the sender’s wallet to the recipient’s wallet on the Ethereum blockchain, with no bank or payment processor in between. A gas fee paid in ETH covers the cost of processing the transaction on the network.

How do I pay with ETH?

You need an Ethereum wallet (MetaMask, Coinbase Wallet, or Trust Wallet), ETH in that wallet, and the recipient’s wallet address or QR code. In your wallet, select Send, enter the address and amount, review the gas fee, and confirm. The transaction typically appears in the recipient’s wallet within 15-30 seconds, with full confirmation in 2-5 minutes for most online purchases.

What stores accept Ethereum as payment?

Major merchants accepting ETH include Overstock (retail), Newegg (electronics), Travala (travel), Chipotle and AMC Theatres (via Flexa), and thousands of Shopify stores through payment processor integrations. PayPal added native ETH payment support in April 2026. Real estate platforms including Propy and Crypto Emporium also accept ETH for property transactions.

Are ETH payments safe?

ETH payments are cryptographically secure – transactions cannot be forged or altered. The main risks are user errors (sending to the wrong address, which is irreversible), gas fee spikes, and price volatility. For buyers, there is no chargeback mechanism if a merchant fails to deliver. Always verify the recipient address before confirming, and for large transfers, send a small test transaction first.

What are the fees for ETH payments?

ETH payments have two potential fee components: the payment processor fee (0-1%, depending on the processor) and the gas fee paid to the Ethereum network ($0.10-$50+ on mainnet, under $0.01 on Layer 2 networks like Arbitrum, Base, or Optimism). For small payments, using a Layer 2 network eliminates the gas fee as a practical barrier.

Can I pay with ETH on PayPal?

Yes, since April 2026. PayPal added native support for sending ETH directly from a PayPal balance to any Ethereum wallet address. Users can also buy, hold, and sell ETH within the PayPal interface. This makes ETH accessible to PayPal’s 400 million active users without requiring them to use a standalone crypto exchange.

Is ETH payment faster than a bank transfer?

Yes, significantly. A domestic bank transfer takes hours to one business day. An international SWIFT wire transfer takes 1-5 business days. An ETH payment on mainnet confirms in 12-15 seconds for initial confirmation and 15 minutes for full finality. On Layer 2 networks, confirmation takes 2-3 seconds. For international transfers specifically, the speed advantage over traditional banking is substantial.